Another subprime lending blowup

H&R Block released the following news late yesterday. I've highlighted some important passages ...

KANSAS CITY, Mo.--(BUSINESS WIRE)--Aug. 24, 2006--H&R Block Inc. today announced that it expects to record a provision for losses of $102.1 million (after-tax amount of $61.3 million or 19 cents per share) reflecting an increase to the estimated recourse liability recorded by Option One Mortgage Corporation for loan repurchases and premium recapture reserves. The expected provision includes $46.1 million related to loans sold during the quarter ended July 31 and an increase of $56.0 million related to loans sold in previous quarters. The Company expects to increase the estimated recourse liability primarily as a result of recent increases in loan repurchases from its loan sale transactions. The increased level of loan repurchases, which have been noted industrywide, are primarily due to a higher level of repurchase requests from loan buyers and an increase in early payment delinquencies.

I've seen the same kind of bad news about defaults and delinquencies from other subprime lenders like FMT and FICC. Frankly, this is a symptom of a problem I've discussed in a number of forums the past several months. Lenders have given too many easy-money mortgages to too many underqualified borrowers for too many overvalued homes. The repercussions could be severe.

You can read a column I wrote a little while back on the topic in our daily MoneyandMarkets e-newsletter. I also shared some insights recently with the New York Sun's Dan Dorfman.

KANSAS CITY, Mo.--(BUSINESS WIRE)--Aug. 24, 2006--H&R Block Inc. today announced that it expects to record a provision for losses of $102.1 million (after-tax amount of $61.3 million or 19 cents per share) reflecting an increase to the estimated recourse liability recorded by Option One Mortgage Corporation for loan repurchases and premium recapture reserves. The expected provision includes $46.1 million related to loans sold during the quarter ended July 31 and an increase of $56.0 million related to loans sold in previous quarters. The Company expects to increase the estimated recourse liability primarily as a result of recent increases in loan repurchases from its loan sale transactions. The increased level of loan repurchases, which have been noted industrywide, are primarily due to a higher level of repurchase requests from loan buyers and an increase in early payment delinquencies.

I've seen the same kind of bad news about defaults and delinquencies from other subprime lenders like FMT and FICC. Frankly, this is a symptom of a problem I've discussed in a number of forums the past several months. Lenders have given too many easy-money mortgages to too many underqualified borrowers for too many overvalued homes. The repercussions could be severe.

You can read a column I wrote a little while back on the topic in our daily MoneyandMarkets e-newsletter. I also shared some insights recently with the New York Sun's Dan Dorfman.

posted by Mike Larson at

10:07 AM

|

0 comments

![]()

![]()

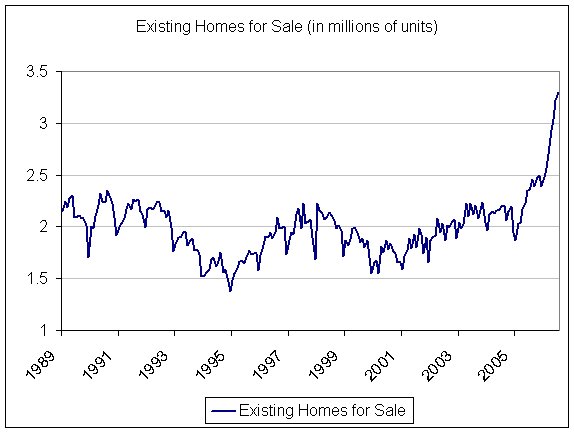

Again, a picture is worth a 1,000 words. This is the quarterly housing affordability index produced by the National Association of Realtors. Notice anything funny? Housing hasn't been this unaffordable since the tail end of the 1980s. And that's with interest rates (long-term ones, anyway) not that far off their lows.

Again, a picture is worth a 1,000 words. This is the quarterly housing affordability index produced by the National Association of Realtors. Notice anything funny? Housing hasn't been this unaffordable since the tail end of the 1980s. And that's with interest rates (long-term ones, anyway) not that far off their lows.

The verdict is still out of course. Maybe the rest of the economy will remain just fine and only the housing sector will suffer a recession. But color me skeptical.

The verdict is still out of course. Maybe the rest of the economy will remain just fine and only the housing sector will suffer a recession. But color me skeptical.